我们不再支持这个浏览器. 使用受支持的浏览器将提供更好的体验.

请 更新浏览器.

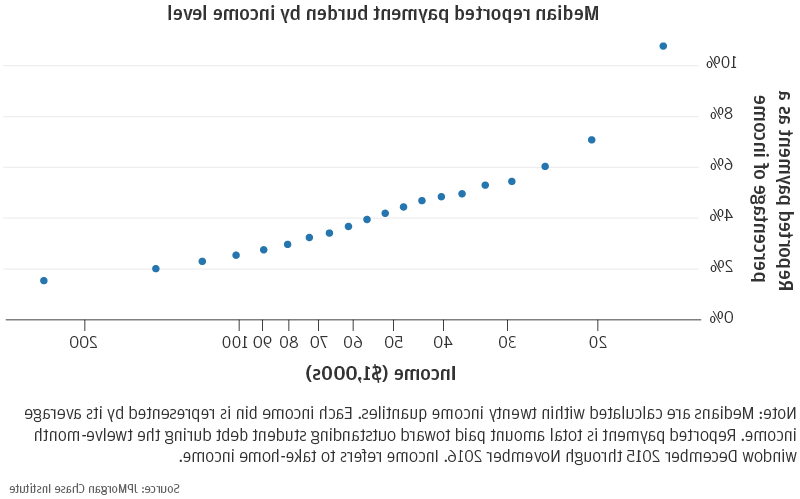

美国家庭携带超过1美元.5万亿的学生贷款债务, 学费也大幅上涨, 增加获得文凭所需的债务数额. 对许多借款人来说, this debt provided the opportunity to pursue higher education with commensurate income keeping debt burdens at reasonable rates. 为他人, 偿还学生贷款仍然是一个潜在的严重经济负担, 与收入相比,学生贷款债务很大.

This report explores how people of different socioeconomic and demographic groups are managing their student debt and potential solutions to student loan debt policy issues. 我们通过链接管理银行数据来做到这一点, 信用局记录的学生贷款数据, 以及有关种族和民族的公共记录,以创建包括收入在内的独特数据资产, 人口统计资料, 债务余额, 还有超过300美元的学生贷款,000人.

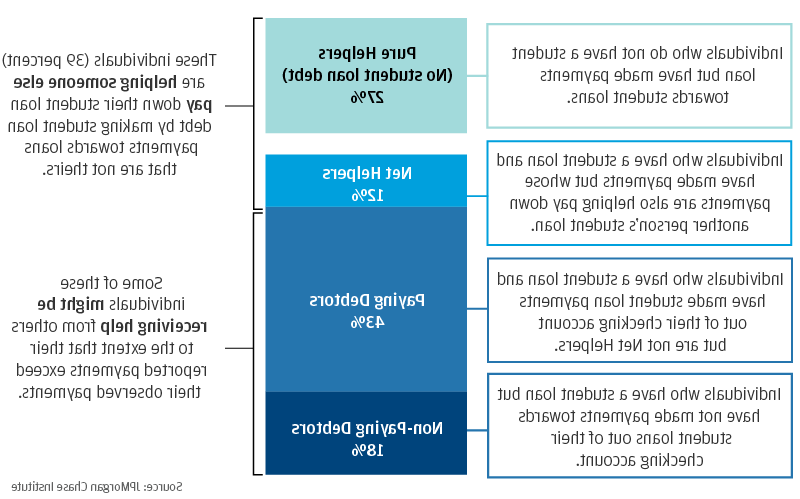

我们发现学生贷款持有人并不是一个单一的群体. 许多借款人并不是不合理地背负着学生贷款的负担,而且还在按时还款. 但是,某些学生贷款群体背负着沉重的债务负担, 尤其是低收入借款人, 老年人, 和黑人借款人. 此外, 我们发现,很大一部分学生债务不是由贷款持有人支付的, 但其他与贷款无关的个人, 可能无法直接收获劳动力市场的家庭成员会从更高的人力资本投资中获得回报. This means that the economic impacts of student debt likely affect a broader portion of the population than previously thought. 另外, the prominent role of help in student loan repayment puts Black borrowers at a disadvantage in that they exhibit a greater unmet need for repayment assistance.

新冠疫情对经济的影响可能会加剧学生贷款债务负担, 特别是对于那些经济上最脆弱的人. While policymakers have taken measures to alleviate some of the short-term challenges by aligning repayment obligations with borrowers’ ability to repay, targeting relief efforts at those most burdened by student debt remains a critical component of continued student loan policy solutions.

应该做些什么来解决我们在学生贷款借款人结果中发现的不同模式? 那是不用说的 抑制学费上涨 学生及其家庭承担的学生贷款债务将从根本上解决问题. 此外, 缩小收入和财富的种族差距 would boost families’ ability to pay for tuition and repay student loan debt among segments of the population most burdened by student loan debt.

先不考虑这些结构性问题这些结构性问题影响了我们观察到的学生贷款偿还模式, 下面我们将探讨几种可能性 有针对性的债务援助项目可以扩大 减轻现有学生贷款借款人的负担. 作为一般原则, 因为大多数借款人都在管理自己的债务,而没有过度负担, efforts to alleviate undue burdens from student loan debt can and should be targeted at those who are experiencing truly difficult conditions. This is true for payment assistance efforts like income-driven repayment (IDR) programs as well as more aggressive actions like debt forgiveness.

扩大有针对性援助的一个相对容易的第一步是 帮助更多借款人更好地利用现有的付款援助计划, 包括收入驱动的还款计划. 这样做的一种方法是减少参与IDR所需的文书工作负担, 例如使年度收入重新认证更容易. 另一个是加大努力,确保借款人了解他们的IDR选择. 我们观察到,至少有10%的人正在支付超过10%的实得收入, IDR程序的通用阈值. We also observe high rates of deferment among low-income borrowers who might be eligible for IDR and eventual loan forgiveness.

然而, 需要注意的是,当前的IDR程序确实有缺点, 新的项目可能是有必要的. IDR只有在成功参与该计划20年后才提供债务减免. 这种延长的时间跨度使得债务减免变得不确定. 参加IDR项目也不是没有风险. 如果借款人减少的还款额少于他们每月的利息, 未付利息将继续累积,而债务本金不会下降. 另外, 如果借款人退出IDR计划, 或者未及时补办年度收入证明的, they will not only be responsible for all the unpaid interest but also for the unpaid interest that may be added to the debt principal and which can begin to accrue additional interest. 很多人在2015年就已经意识到了这一风险, 在IDR项目中,57%的借款人未能及时重新证明其收入(Department of Education, 2015)。.

我们的研究结果强调 current student loan debt policies and assistance programs may not adequately consider the network of people the borrower may rely on to make their payments. This means that a borrower’s income statement may understate both her ability to pay and her vulnerability to job losses and financial disruptions among her financial support network. 这个问题有可能使代际财富不平等永久化,给父母带来不应有的负担. 对于有钱的父母, 通过支付学费或偿还学生贷款来资助教育是将财富转移给下一代的一种方式. 对于不太富裕的父母, 如果他们不能从孩子的收入补贴中受益,偿还学生贷款债务将是一个额外的经济负担.

学生贷款政策应该考虑到这些家庭动态. 首先, 贷款发放计划可能需要重新平衡学生和家长之间的贷款资格. 目前的贷款发放项目明确区分了借款人和他们的父母. 例如, 联邦家长贷款, 哪些是由受抚养大学生的父母代表他们的孩子拿出来的, 是否比直接提供给本科生的贷款利率和限额更高. We observe younger borrowers making payments on loans that are not in their name and older borrowers receiving help with their loans, 其中大部分是家长PLUS贷款. 这表明许多学生正在偿还父母的贷款. 如果这些贷款最终由学生自己支付,对再分配的影响是什么? 贷款限额是否应该提高,以使学生正式承担更多的债务, 让他们获得较低的利率和当前的支付援助计划?

第二,也许 应该有更多为父母设计的支付援助渠道. 使用Parent PLUS贷款等工具的借款人不符合IDR等项目的资格. 这就给那些替孩子借钱的父母制造了一个潜在的陷阱. 如果学生完成大学学业并获得收入溢价, 他们可以通过父母贷款来帮助父母. 我们对高级借款人获得大量帮助的观察表明,这可能是一种常见做法. 然而, 如果学生不能获得足够的奖励, 他们可以得到一些援助, 像印尼盾, 但可能无法帮助他们的父母,因为他们没有任何途径可以获得帮助. 有相当一部分美国老年人参与助学贷款偿还,但进展非常缓慢, 他们的债务负担很可能一直延续到退休.

偿还救济计划的一个可能的补充是 允许通过类似破产的程序重组或免除学生债务. 目前, student debt is only dischargeable under Chapter 13 (debt restructuring) when a debtor can convince a judge that they have extreme economic hardship and if the debtor completes a 严格的五年还款计划. 在实践中,这种情况很少发生. Enabling student debt to be discharged might ultimately increase the cost of borrowing to the extent that the existence of the policy changes default rates. Targeting discharge—for example to those with limited assets and have been in default for several years— could mitigate these price effects.

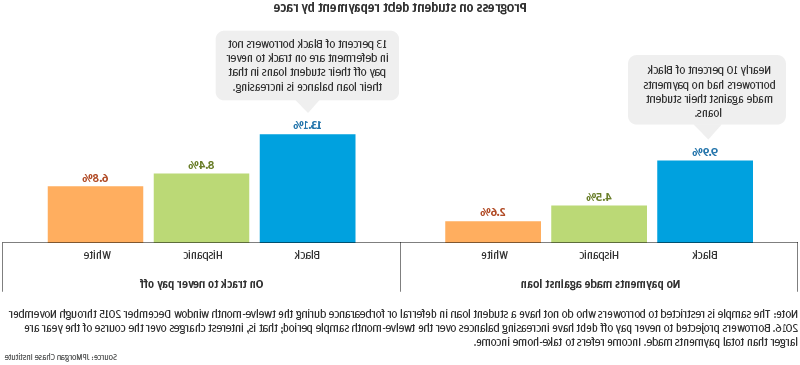

解决不当支付负担的另一个步骤是 加大力度,为负担最重的人提供有针对性的债务减免. Although debt relief is available for graduates entering certain careers and for those who remain in an IDR program for twenty years, 我们的证据表明,有机会扩大有针对性的债务减免渠道. We find that a higher share of lower-income 和黑人借款人 face extreme payment burdens (over 10 percent of take-home income) and are projected to never finish paying off their loans if current repayment trends continue. 鉴于黑人和西班牙裔家庭在劳动力市场上面临着不成比例的结构性挑战, 有强有力的证据表明在收入方面存在种族差距(法雷尔等人). 2020). 因此, 黑人和西班牙裔毕业生的教育回报可能低于白人毕业生, 这使得黑人和西班牙裔借款人有效偿还学生贷款变得更具挑战性. Targeted student loan debt forgiveness could be a means of rebalancing our investments in public goods like education across communities and insuring against the risk that borrowers, 黑人和西班牙裔借款人比例过高, 发现自己陷入债务陷阱.