我们不再支持这个浏览器. 使用受支持的浏览器将提供更好的体验.

请 更新浏览器.

The Great Recession brought to the forefront many unanswered questions about how monetary policy plays out at a microeconomic level, notably the question of how changes in the federal funds target rate impact personal consumption for individual households. 不足为奇的是, this question is difficult to answer because of the multitude and variety of financing products and constantly evolving market conditions, as well as the paucity of data integrating financing terms with consumption at the household level over time. 在澳博官方网站app研究所的这份新报告中, we turn to a sample of homeowners who hold a specific type of mortgage particularly sensitive to interest rate changes to inform this question in an innovative way.

We examine how a sample of US homeowners changed their credit card spending in response to a predictable drop in their mortgage payment driven by the Federal Reserve’s low interest rate policy that followed the Great Recession. Using a de-identified sample of 追逐 customers who had hybrid adjustable-rate mortgages (ARMs) and a 追逐 credit card, we analyze changes in credit card spending and revolving balance leading up to and after mortgage reset.

在ARM复位之前的12个月, credit card spending increased by 9 percent ($289 per month) on average relative to spending in the baseline month (12 months before reset). 重要的是, 这笔支出发生在抵押贷款支付减少之前, 这是一种预期的反应. 重置后的12个月内, spending increased by 15 percent ($488 per month) on average relative to spending in the baseline month.

这些房主增加了他们的支出,尽管近84美元,000(25%),他们的房屋价值中位数下降,贷款与价值比率相应上升, indicating that the decrease in housing wealth and ensuing increase in household leverage did not prevent them from increasing their spending in response to a boost in income.

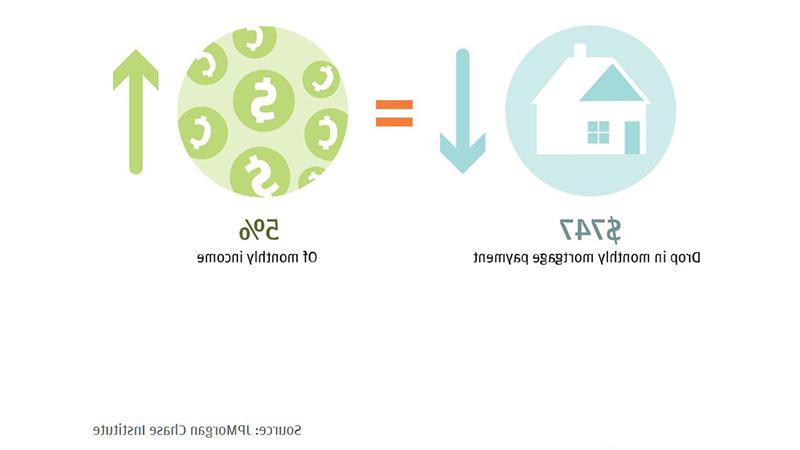

平均, homeowners in our sample used $741 of credit card borrowing in the pre-reset period to smooth the increase in their consumption before income actually increased. The $741 increase in revolving balance suggests they financed 21 percent of their pre-reset spending increase.

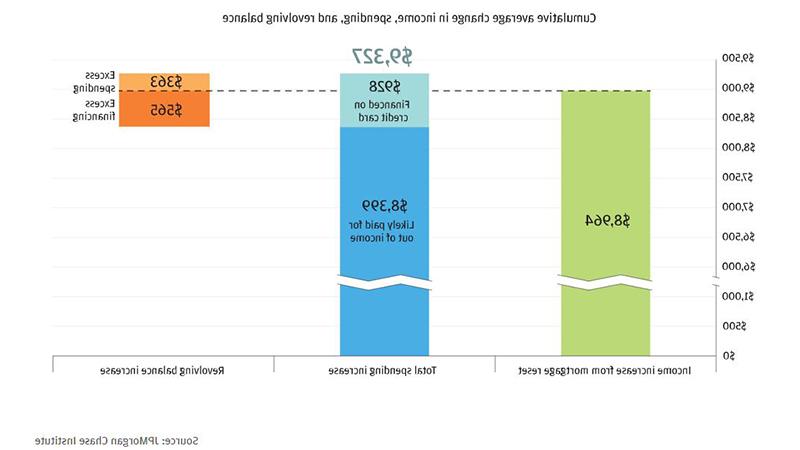

在整个两年期间, the average revolving balance increased by $928 and the total spending increase actually exceeded the total savings from mortgage reset by 4 percent ($363). Comparing the $928 increase in revolving balance to the $363 of excess spending suggests that these households could have reduced their revolving balances by $565 at the end of the period without changing their credit card spending levels over the prior 24 months.

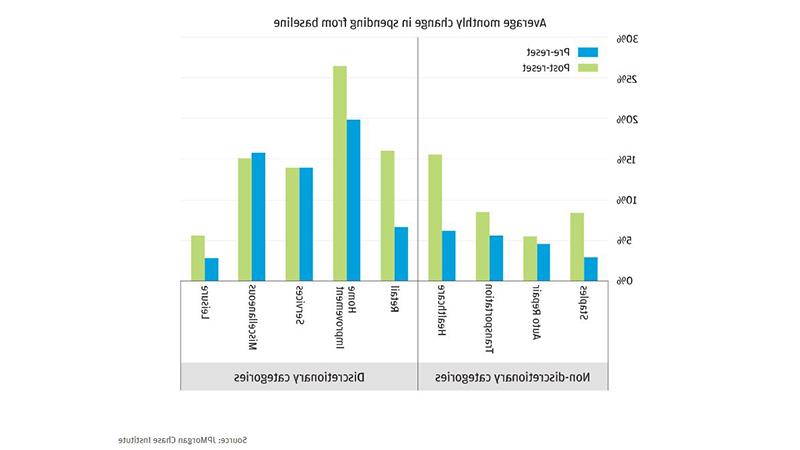

在重置前和重置后期间, spending increased in every category and the discretionary spending increase exceeded the non-discretionary spending increase.

在可自由支配的消费中,家庭装修支出增长最多. This is particularly noteworthy as it represents an increased investment in a leveraged asset just after the asset lost 25 percent of its value.

在非必需采购范围内, 医疗保健支出大幅增加,但这只是在重置后的时期, 建议房主推迟医疗支出,直到收入增加成为现实.

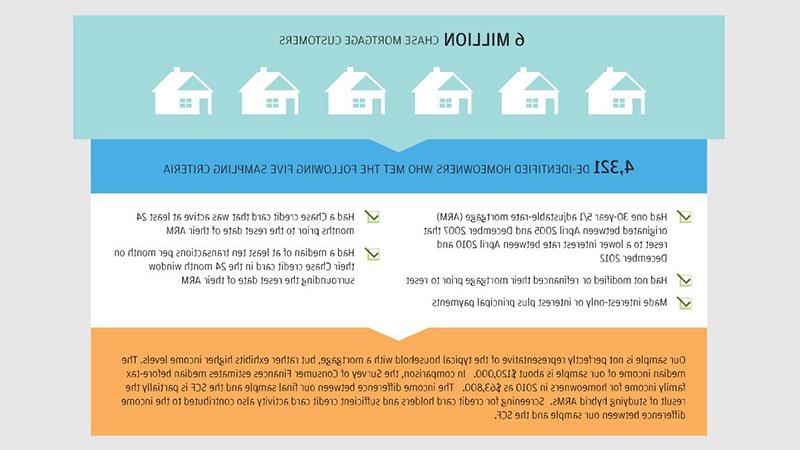

从600多万大通银行的抵押贷款客户中, 我们创建了4个样本,符合以下五项抽样标准的321名去识别房主:

货币政策通过多种渠道影响经济, 每个渠道的有效性在宽松和紧缩周期中有所不同. In this report we measure the effects of the income channel of monetary policy on the consumption of homeowners with a specific type of variable-rate mortgage. 我们发现,在利率下降的环境下, 收入渠道是自动的, 消费者的反应相当可观, 消费的增长既有预期的,也有同期的. To put our findings in the broader context of the monetary policy transmission channels that operate through mortgages to impact personal consumption, we turn to research that shows that the refinancing channel suffers from shortcomings that limit its impact on homeowners: it is difficult to activate with conventional interest rate policy, 摩擦会减少它的带宽吗, 而且有不均衡的分配效应.

重要的是, housing policy that influences the share of fixed-rate mortgages versus variable-rate mortgages will partially determine the share of homeowners that will be impacted by the refinancing channel versus the income channel and therefore will also impact the overall effectiveness of monetary policy. 像这样, when housing policy makers evaluate the policies that influence which type of mortgage (fixed-rate or variable-rate) borrowers choose, they should consider the effects these policies will have on the ability of monetary policy to impact personal consumption through the business cycle.